.svg)

.svg)

.svg)

How to get in-network coverage for out-of-network medical treatment

This guide could save you $30,000+ and allow you to go to a top surgeon or other medical provider, depending on the medical treatment you need.

Health insurance companies often pay less than 10% of the price for out-of-network treatment, leaving patients with over 90% of the bill (which, for many surgeries, is tens of thousands of dollars). Many patients wrongly assume that insurers will pay most of the bill, but they don’t realize until after their treatment that their insurer will pay so little. And on top of that, patients don’t know that they could have appealed to their insurer for in-network coverage for that out-of-network treatment in the first place. This means that insurers are covering based on the provider’s billed fees, not their “allowable amount.”

It’s possible to pay the same amount for out-of-network treatment as you would pay in-network, but it requires you to appeal to your insurer. This guide explains how.

But, remember: there are no guarantees; success depends on your specific procedure and insurance company. These appeals can be difficult to win. It’s possible, but not guaranteed. See more information on this in the first section directly below.

Quick note on wording: our use of the word “appeal” refers to any form of written advocacy to your insurer. Physicians and insurers, who typically only write and read appeals for medical necessity, will think the term “appeal” only refers to getting a treatment “approved.” However, this guide goes beyond getting the treatment approved; it discusses how to get in-network coverage if it’s out-of-network.

Disclaimer: The information provided on this website is intended for general informational purposes only and does not constitute medical or legal advice. We are not medical professionals, nor are we attorneys.

If you only read one thing, make it this section

Here is the most critical information that 99% of patients don’t know:

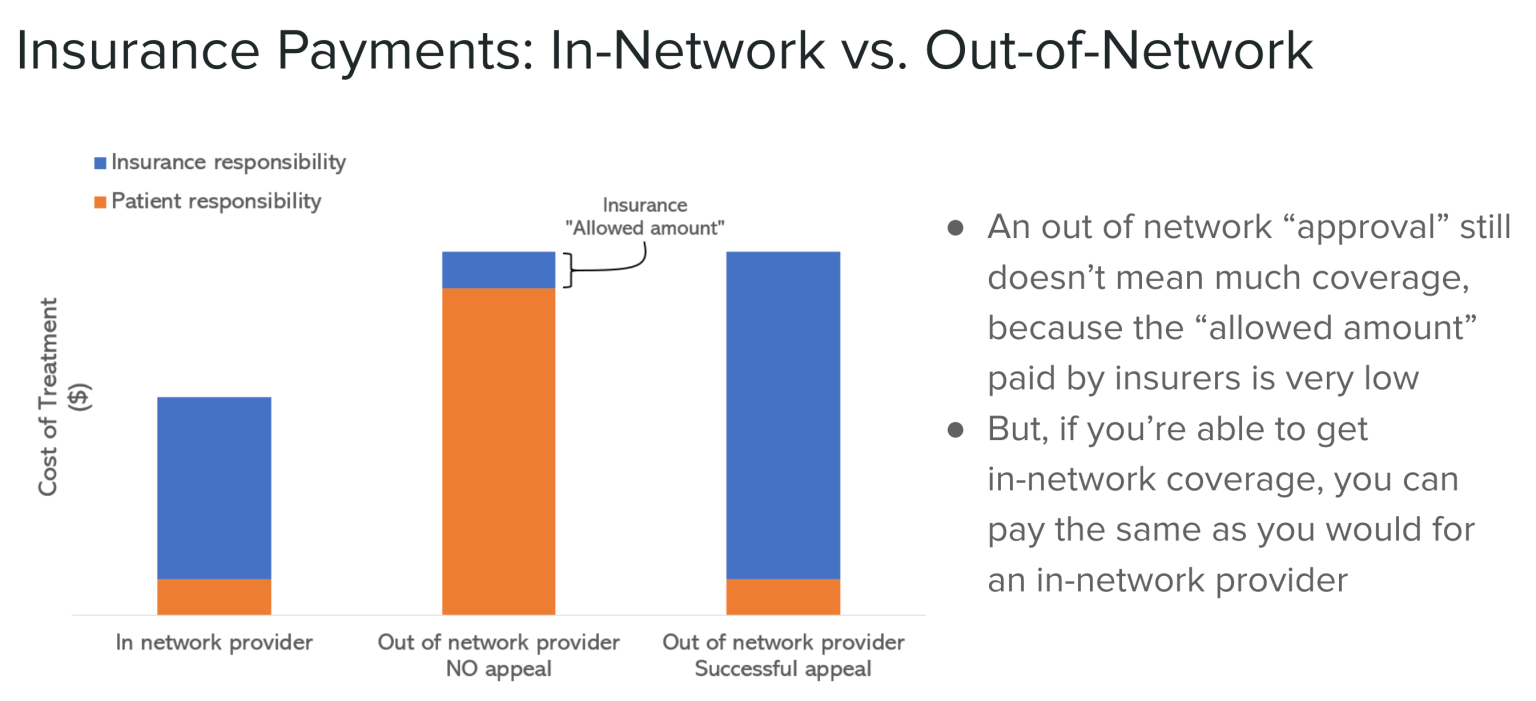

- Insurers pay very low amounts for out-of-network medical treatment, often less than 10%. Their payments are lower than what they normally pay surgeons in-network, even though out-of-network treatment often costs more. (See graph below.)

- Patients can appeal to their insurance company for better coverage. You make the argument that the care you need is not available in the network; see the last section of this guide for more on that.

- It’s best to appeal to insurance companies before your treatment rather than after, based on the internal processes that insurance companies use to handle these cases.

There are no guarantees of winning the appeal, but the amount of money at stake means it’s likely worth appealing for major surgeries and other expensive treatments, even if you don’t think you’re likely to win.

Here is how it works:

When you go out of network, insurers can claim the provider’s billed fees are over the allowed amount, and that typically leaves the patient responsible for the balance billed charges (i.e. the difference between the allowed amount and the billed fees). Here’s an example:

- You have an in-network out of pocket max of $2,000, and an out-of-network out of pocket max of $4,000.

- You go to an out of network surgeon who is performing the treatment at an in-network hospital

- The out of network surgeon has surgeon’s fees of $50,000, and the in-network hospital fees are $120,000

- You agree to pre-pay the out of network surgeon’s fees of $50,000, and sign a form saying you’ll be responsible for dealing with insurance and appealing for reimbursement

- You have the surgery

- You receive the Explanation of Benefits one month after the surgery

- Hospital fees: your insurance covered $118,000 and you paid the $2,000 in-network out of pocket max

- Surgeon’s fees: your insurance claims their allowed amount for the procedure is $3,000. Therefore, you are responsible for the remaining $47,000.

Unfortunately, insurers are many times able to get away with this, but it is still worth trying to see if they will make an exception for your case, and if you do win, they will usually at least increase your reimbursement by some amount.

There is significant variance in how much money insurers will offer for out-of-network treatment in cases when in-network surgeons aren’t available. Sometimes insurers offer barely more than the in-network contracted rate, which you should also appeal against.

Always get in writing how much they plan to cover, so there are no surprises later.

What if my appeal fails and I can’t afford out-of-network surgery without additional coverage?

One option that some clients pursue is to appeal for in-network coverage with an out-of-network provider first, and then go with an in-network surgeon if the appeal fails. Of course, this means it could take longer to get the surgery done, but the top in-network surgeons (such as those at university hospitals) often have long wait-times anyway, so you could book an appointment with them and pursue the out-of-network surgery option with your insurer in the meantime. If you do this, just make sure the out-of-network surgeon submits the prior authorization first and the in-network surgeon doesn’t start the prior authorization process until you’ve exhausted your options with the out-of-network surgeon. The costs of consultation appointments vary by surgeon and insurance plan (although it’s always significantly less than for the surgery itself), so you’ll want to check your plan and their prices to ensure this isn’t too much of a financial burden.

See chart below for typical coverage proportions. Insurers will typically foot the bill for most of the treatment when it’s in-network, but they’ll pay significantly less for out-of-network treatment. With proper appealing, you might be granted an exception to pay the same amount for an out-of-network treatment as you would in-network. This means, in other words, that insurers would cover the treatment based on the provider’s billed fees, not their “allowable amount.”

We directly help patients advocate to their health insurers to pay in-network rates for out-of-network doctors and treatment.

.svg)

Choosing the right provider: in-network vs. out-of-network

Note that we are not advising to go with one provider or another. Rather, we are giving information about the overall healthcare landscape so patients can make their own decisions.

Many patients choose out-of-network medical providers (especially surgeons) for the following reasons:

- “Cash pay” surgeons who are out-of-network with all insurance plans tend to be the most experienced. They can charge high prices (and don’t need to be in-network with any insurance plans) because there is significant demand for their services from patients. For patients, a surgeon’s experience might matter when the surgery is highly specialized or complex.

- Many in-network surgeons might not perform a specific procedure very often. For example, many oral surgeons will do 1-2 double jaw surgeries per month, and many patients needing double jaw surgery are more comfortable with surgeons who perform this procedure multiple times per week.

- Some specialized procedures might only be performed by out-of-network surgeons. For example, the EASE procedure is only performed by Dr. Kasey Li, who is out-of-network with all insurers. In these cases, the odds of winning an appeal could go up, given that there are by definition no in-network providers (see below section on writing the appeal).

Again, it’s possible to pursue the out-of-network option first and go back to the in-network option if the out-of-network appeal fails, as long as you can risk possibly getting the treatment later than you otherwise would. See relevant expandable blurb in the above section for more information.

The process to get coverage for out-of-network treatment

Here are the general steps you can take.

Step 1: Ensure that your insurance plan allows for out-of-network care

Note that this guide is written for patients in the United States. If you don’t have health insurance in the United States, the general principles throughout this guide will likely apply, but the setup of your insurer (and the odds of succeeding in getting coverage for an out-of-network provider) will vary. Email us with questions: info@paxoshealth.com.

First, figure out what type of insurance plan you have. You might have a “preferred provider organization” (PPO) plan, “exclusive provider organization” (EPO) plan, or “health maintenance organization” (HMO) plan. PPO plans typically allow for out-of-network care, and other insurance plans (such as EPOs and HMOs, see below) won’t pay anything out-of-network in most cases, unless it can be demonstrated that no surgeon in-network is qualified (more on that in the next section). Appealing for strong coverage of out-of-network surgery is possible in EPO and HMO plans, but you’re usually less likely to succeed than with a PPO plan.

Step 2: Your out-of-network surgeon submits a “prior authorization” claim to your insurer

Prior authorization is a process where a healthcare provider gets approval from an insurance company before providing certain medical services, treatments, or medications to a patient. Prior authorizations are typically required for any treatment of at least moderate cost, including most surgeries.

Your treatment provider will typically submit this claim on your behalf (which contains your medical information and a justification for the treatment) even if they aren’t in-network with any insurers (e.g. they’re “cash pay”). Providers can also “appeal” denials of the treatment from the insurer (like if the insurer claims the treatment isn’t medically necessary), usually without the patient being involved. But, once the treatment is approved, there’s nothing more your provider can do to make insurers pay more than their “allowable amount” for the out-of-network treatment. That’s where this guide comes in; see next step.

What is the “allowable amount” that insurers will pay for out-of-network treatment?

The phrase “allowable amount” typically means the amount that an insurance company will pay for an out-of-network treatment in a geographical area. For out-of-network surgeries, for example, it’s usually <10% of the price for that surgery.

This is usually based on what Medicare pays for a service, and that tends to be lower than what commercial health insurance companies pay for that treatment. In other words, by default, health insurance companies pay less of their own money for out-of-network treatment than they pay in-network.

The “allowable amount” often used to be called the “usual and customary fee,” but it has changed in recent years, likely because the amounts decreased and insurers can’t justify these paltry amounts as usual and customary any more.

If your provider can’t overturn an insurance denial (i.e. insurers claim it’s “not medically necessary”), then you as the patient can appeal that denial. For more on that, see our comprehensive guide for patients on how to write appeals. But note, if your provider is out-of-network, this “medical necessity” appeal is a separate step from appealing for out-of-network coverage; you’ll need to do that too after it’s been approved.

Step 3: You appeal to your insurer for in-network coverage of your out-of-network procedure

Most patients never reach this step, but they should given that there could be tens of thousands of dollars on the line. However, if you call your insurer to ask about this, the representative will likely have no idea what you’re talking about because it isn’t common for patients to write these appeals.

Basically, you write and submit a “request for reconsideration.” You shouldn’t call it an “appeal,” because when insurers hear the word appeal, they’ll think you’re arguing that the procedure is medically necessary, which they’ve already determined it to be if you’ve reached this step. See next section on how to write these requests for reconsideration.

What happens after patients submit the request for reconsideration?

When you submit this request for reconsideration, your insurer will usually take a long time to review it. The “letter of medical necessity” mentioned above will help expedite the process.

First, insurers will evaluate the claims made in your request. Usually, if they really do consider it and there truly are reasons you can’t get in-network care, they’ll consider letting you go out-of-network. But sometimes, your request doesn’t get anywhere beyond the low-level administrators and they just deny it in a way that shows they clearly haven’t read it, in which case you need to appeal again with stronger language and call them directly to stress that this request needs actual review.

Once they agree that there isn’t anyone in-network, insurers will attempt to negotiate with the provider to form what’s called a “single-case agreement” (SCA) on what they pay the provider for your case. The provider might or might not agree to this SCA, but even if they don’t agree, your insurer might still cover your procedure such that you only pay as if it were in-network. This part of the process is quite opaque, and insurers will have a range of responses.

If the scheduled date for your treatment is approaching, a doctor can write you a “letter of medical urgency.” Otherwise, insurance companies usually take 15-60 days to review your request. This letter of medical urgency states that it is medically necessary for you to get this request reviewed quickly given that treatment depends on it, and it often means that insurers are required to make a decision within 72 hours. Ideally, your treatment provider can write this letter, but if they won’t, try to get your primary care physician to write it. This letter just serves to expedite your case within your insurer’s process (getting it into a “different queue”); you don’t need to prove your case in this letter.

There is significant variance in how much money insurers will offer for out-of-network treatment in cases when in-network surgeons aren’t available. Sometimes insurers offer barely more than the in-network rate, which you should also appeal against.

Always get in writing how much they plan to cover, so there are no surprises later.

Step 4: If Step 3 fails, you appeal to other parties overseeing the insurer

If your request for reconsideration doesn’t work, you have other options available. (Our service handles these for clients with no additional fee when our initial appeal fails). You can consider the following:

- Submit another letter to your insurer. Many insurers have processes where another individual not involved in the initial adverse determination will review the case.

- If you’re on a self-funded plan, you can submit an appeal to your employer. A self-funded insurance plan is a health insurance arrangement where the employer pays for employees’ medical expenses directly and the insurance company just handles the administration; this means your employer can “overturn” the adverse decision from the insurance company. Many employers (especially large employers) are on self-funded plans, but their employees usually don’t know. To find out whether you’re in a self-funded plan, you can ask your HR department, although usually you’ll need to reach someone in HR who is involved in the health plan, as this isn’t common knowledge. Your employer might be more likely to grant you your exception than the insurance company, especially with a long and in-depth appeal.

- You can appeal to regulators who oversee the insurer. This gets complicated, because the exact regulator varies between insurance plans, and regulators who don’t directly oversee your insurance plan won’t be able to help or review your case. Typically, self-funded plans (as described above) are overseen by the Employee Benefits Security Administration (EBSA) at the national-level, and fully-funded “regular” insurance plans are overseen by an insurance commission in your state. (We can help you determine which applies to you; just reach out to us: info@paxoshealth.com.) But remember: often with these external regulator reviews, you only get one chance, and if they make a decision in favor of your insurer, you might be fully out-of-luck.

We directly help patients advocate to their health insurers to pay in-network rates for out-of-network doctors and treatment.

How to write your request for reconsideration

Let’s start with a few high-level notes:

- It’s quite difficult to explain exactly how to organize these appeals because it varies so much case-by-case; this is why we haven’t included a one-size-fits-all template in this guide. But, we’ve included general principles here, and you can fill out the intake form on our homepage to get more information.

- The appeals you write should be very comprehensive; the ones we write are typically 20+ pages single-spaced (some are 100+ pages!). It takes a significant amount of work, including research; if you’re debating including something, you should include it.

- We also offer a service to write these appeals for you where you only pay us if we win, and we guide you on submission strategy and write follow-up appeals if necessary (no extra charge). We have a library of precedent cases and legal regulations (see below for how those fit into the appeals) to draw from. See more on our service here.

Insurance companies will view this as a contractual dispute. As such…

- Don’t include emotional arguments, such as “I deserve healthcare,” etc. They won’t work, again because insurers view this as a contractual dispute.

- Don’t argue that their policy is unfair. You (or your employer) signed the contract for it already. Instead, you should argue that the policy should be applied differently in your case.

Your request to them should be for coverage based on your provider’s billed fees. Otherwise, they might just pay their allowable amount, which will likely be significantly lower than the provider’s billed fees.

Your main strategy is to argue that there is no equivalent care in-network for your specific case. This is the cornerstone component of your appeal. In a general sense:

- Understand what’s complicated/different about your case compared to others seeking the same treatment. Do you have additional health issues that require specialized care? Do you need a specific variant of a surgery that most surgeons don’t perform? Note that cosmetic concerns will generally not be considered by your insurer.

- Use your provider’s website to understand their qualifications to perform your procedure. Notice ways in which their qualifications are special (if you’re going with an expert in the field, this shouldn’t be difficult).

- Get a list of in-network options in your location (which can be provided by your insurer). You can find the in-network options by determining the location radius that your insurer will require you to travel, then call all of the in-network offices within that radius that supposedly perform this procedure. The insurance company directory will probably be out of date anyway, and it might not be difficult to find reasons why each in-network doctor is unqualified. Do the comparison of the body of work (i.e. medical literature on PubMed) between providers.

Other components to include in the appeal (which again, should ideally be 20+ pages if you’re covering everything):

- A summary at the beginning of the document highlighting all salient points; this will ensure that readers get the full gist of it even if they don’t read the whole thing. For more on how to organize a document, see our comprehensive appeal-writing guide.

- Letter of medical urgency from your physician, as explained in the above section. This should also be sent by them to your insurer separately, but an additional copy in your appeal will show reviewers that they need to act quickly.

- Any provisions your insurer has on out-of-network care coverage. For example, perhaps some part of the policy plays in your favor. These morsels usually appear in the Plan Document; the Plan Document explains your insurance plan’s entire medical policy to you; it should be 80+ pages (not the short booklet; that’s a different document), and it can be called a variety of names including “medical benefits booklets,” etc. Insurers will often delay or avoid sending this document, but they’re required by law to provide you with it in a timely manner. We recommend (politely) reminding them of this when you’re on the phone with a representative; it’s fair to ask for those documents within one business day.

- Cases where you know of previous patients that got in-network rates for out-of-network surgery. This will help showcase that they need to grant you the same exception that they’ve granted others before. (For example, we have a library of precedent from the previous cases we’ve worked on.)

- Relevant regulations and published guidelines governing insurance companies that could apply to your case. Unfortunately, this is extremely complicated. Make sure that the regulation applies to your specific plan (see above section on self-funded vs. fully-funded plans), because the legal landscape varies around the United States for different insurance plans.

- Remind them of the medical necessity of the case. At this stage, they’ve already approved it in a general sense, i.e. they would provide coverage for an in-network provider (if they haven’t approved it, see our guide on appealing for approval in the first place), but it is worth recapping why this is necessary. Here you can also harp on the complexity of your specific case, hence why you can’t get the needed care in the network.

- Include ways in which your insurer has mishandled the case so far, for good measure. While this won’t win them over on its own, the additional color provided could encourage individuals who see it to act in your favor.

Describe any of the following that could apply. If you have specific dates, even better (but no worries if you don’t).

- Instances when you were given erroneous information

- Delay or failure to furnish documentation that they’re obligated to provide

- Non-returned phone calls from the insurance company

- Times when you were passed around customer service with no good answers

- Outdated in-network provider directory (this applies in almost every case)

- Missed deadlines (for example, if they didn’t review something in time).

Remember: make sure to find out the amount they’ll pay before surgery. Otherwise, you risk misunderstandings later.

We wrote an entire guide on writing appeals, check it out here. You can also check out our service where we only charge a fee if we win you coverage.

Send us questions and feedback via email (info@paxoshealth.com); we’ll update this guide continuously. As mentioned above, we can also help you write your appeals to maximize your chances of success.

Disclaimer: The information provided on this website is intended for general informational purposes only and does not constitute medical or legal advice. We are not medical professionals, nor are we attorneys. While we strive to provide accurate and up-to-date information, it is crucial to understand that each case is unique and may require specialized expertise. Do not rely solely on the content found here for making decisions regarding your health or legal matters. Always seek the advice of licensed professionals when dealing with such matters.